11 Practical Accounting concepts for Equities Futures Derivative

Learn accounting for equities futures derivative(F&O), save the penalty, interest, prepare your books of account, present it in the ITR, independently.

One fine day I received a call from a salaried employee, also a trader in Equities Futures Derivative, who received a penalty notice of Rs.25,000/- u/s 271A from the Income Tax Department. He was not sure of the reason for such penalty, as he had paid tax on his salary, interest income and Equities Futures Derivative Profit, while filing his return of Income. I immediately asked him to forward all his documents to have a closer look at his transactions.

On screening through, I noticed that he had traded in Equities Futures Derivative, and was under mandatory requirement to maintain his books of account and file return of income with relevant details, due to his derivative income exceeding basic exemption limit and/or Turnover limits.

There are some other cases, who received scrutiny notices for not complying with audit provisions and mandatory requirement of Books of Account in case of loss.

Paying penalty or attending to scrutiny, was unnecessary and I felt accounting independence is the need of the hour.

While solving this case, I thought to myself, that there might be many more who might be in such a situation and accounting independence can help them save such penalties and scrutiny, prepare their own books of account and be 100%, statutory tax compliant.

What if I told you that you can save Rs.18,000/- or more every year, by learning and implementing accounting for Equities futures derivative(F&O) for your own Business Income, from anywhere without being dependent on anyone.

You can also save a Penalty of Rs.25,000/- every year and

Save Interest payments of approximately 10% on your Net Tax Liability.

Will you be interested to read further about your accounting independence?

When I say accounting, you might think of it as recording journal entries, posting to ledgers, preparing trial balance, and then finally preparing final accounts.

This process of traditional accounting is now transformed into the direct preparation of final accounts through simple importing of bank statements and ledger into the software, from anywhere, at the click of a button and after classifying transactions under five different heads, prior to importing.

Presentation of Equities Futures Derivative transactions in financial statements, computing your income, and the presentation in the Return of Income, practically and independently, will earn you Accounting Independence.

You will be able to control your losses, increase your profits, manage the fund’s positions, and keep a track of ledger balances in the initial margin deposits against which you can take respective positions in the equity’s futures derivative markets, through continuous monitoring of your financial statements.

Trading and accounting in Equities Futures Derivative(F&O) is not unique these days. Many finance professionals including Salaried employees are dealing in Equities Futures Derivative or F&O in India.

Income from Equities Futures Derivative(F&O) is taxable under the head “Income from Business and Profession”.

Accounting treatment, its presentation in financial statements and in Income Tax returns need some understanding.

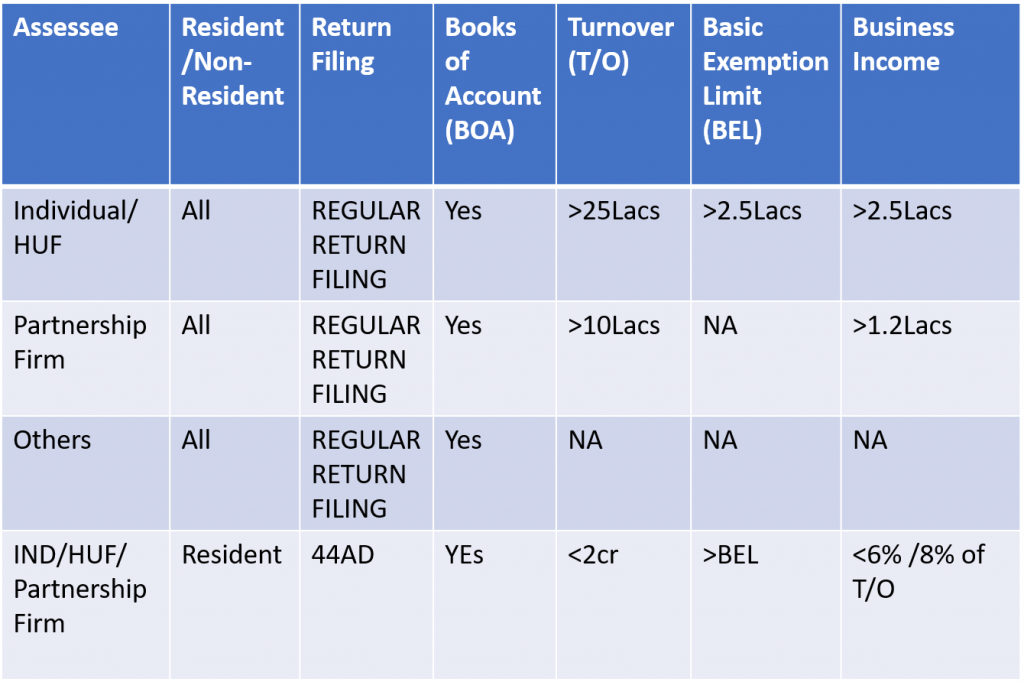

On the basis of Books of Accounts, the turnover and Business Income can be ascertained, on the basis of which you can decide whether you are eligible for a tax audit, or may opt for Sec 44AD, or can file regular Income Tax returns.

Let us understand 11 practical accounting concepts in the preparation of financial statements, and computation of income with examples.

What is Accounting and Books of Account?

Mandatory maintenance of Books of Accounts

Books of account mainly comprise of preparing Journals, Ledgers and Trial Balance, before finally preparing Profit/Loss a/c, Balance Sheet. Every person carrying on business has to compulsorily maintain books of Accounts, in case of Individual/HUF, if your Turnover exceeds Rs.25lacs or Business Income exceeds Rs.2.5Lacs and in case of Partnership Firms, If Turnover exceeds Rs.10Lacs or Business Income Exceeds Rs.1.2Lacs and in all other cases, it is mandatory to maintain books of accounts without any basic limit, as explained in the following case,

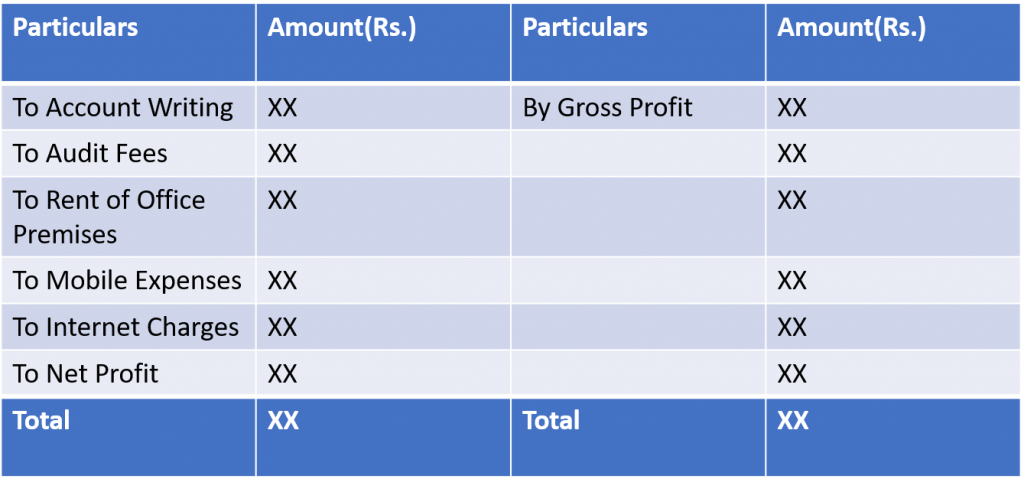

Presentation in Books of Account

All Business Income is posted as income/loss in Trading Account, and Initial Margin, ledger balances in the balance sheet. You can claim various expenses such as Salary paid, Audit Fees paid, Utility expenses, Printing & Stationery, Rent paid, Depreciation in the Profit/Loss account. The balances as of 31st March will be presented in the Balance Sheet.

Following is the proforma of Books of Account for your easy reference.

Trading A/c for the year ended 31st March 2022

Profit & Loss Account for the year ended 31st March 2022

Balance Sheet as on 31st March 2022.

Why is it important to prepare Financial Statements?

Preparation of Financial Statements will help you to determine whether you are eligible for a tax audit or can claim the benefit of Presumptive taxation or file regular returns of Income.

Tax Audit

If your Business Income and/or F&O trading income, is a Loss or turnover is more than 10Crores/1crore, or above Basic Exemption limit, Or below 6%/8% of the turnover in case of presumptive taxation, as the case may be, your books of account prepared needs to be audited by a Chartered Accountant, in order to ensure that all the figures mentioned in the Books of accounts give a true and fair view of financial statements/position prepared.

You can claim set-off of Equities Futures Derivative loss against all other Income except Salary Income and pay tax only on the balance Taxable Total income.

Sec 44AD- Presumptive Taxation benefit

Every Individual/HUF/Partnership Firm, an Eligible assessee, being small taxpayers doing business (including Equities futures derivative (F&O) trading), is given a benefit of presumptive taxation, wherein only 6%/8% of the Turnover is computed as your Business Income for a turnover up to Rs.2crores. Business such as commission agents, or plying or hiring of goods carriages is outside the purview of Sec 44AD.

Regular Income Tax Returns

IF your Turnover is up to Rs.10 crores, and above Rs.2 Crores, you can file your regular income tax returns without tax audit, after preparation of your books of account. For Business Income up to Rs.2 crores, you can avail the option of either presumptive taxation u/s 44AD or file regular income tax returns after preparing your Profit & Loss, Balance Sheet.

4 practical accounting concepts to determine your accounting requirement.

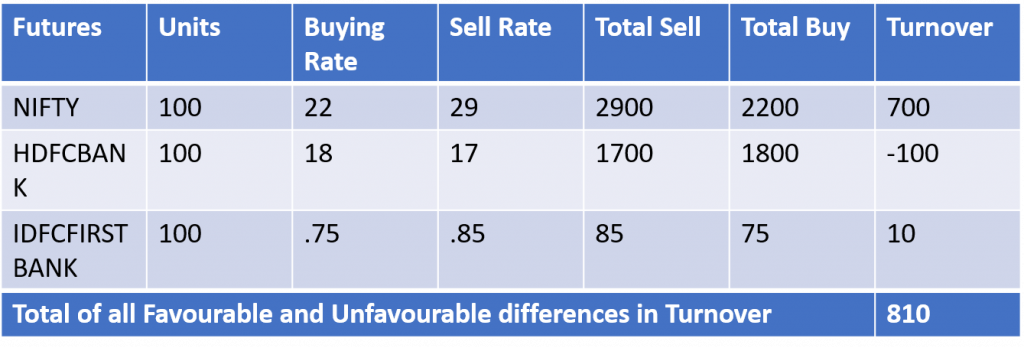

Calculation of Turnover

The Turnover is calculated as the total of all the Favorable and Unfavorable differences in the Turnover. Books of account have to be maintained mandatorily if the turnover crosses 25Lacs/10lacs in case of individual, HUF, Partnership Firms respectively.

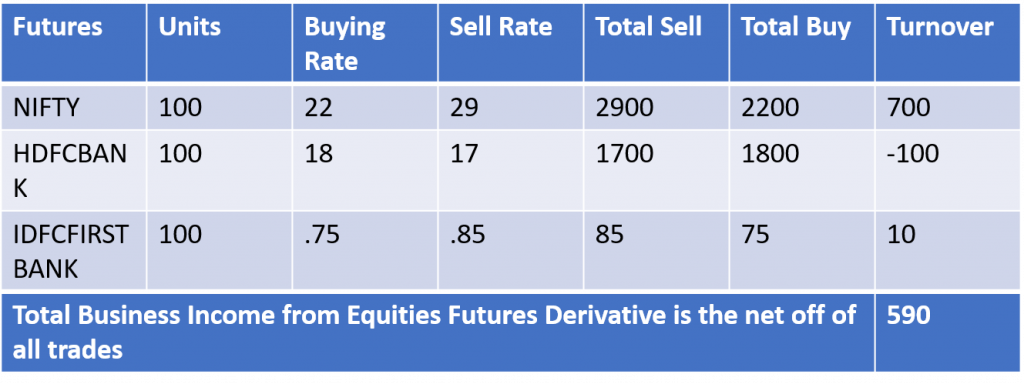

Business Income

Business Income is obtained through netting off the difference between all trades, Mark to Market at the end of each day. Business Income is the amount which is finally reflected in your Computation of Income and is of utmost importance. Mandatory books of account is to be maintained, if Business Income exceeds 1.2Lacs/2.5Lacs in case of Partnership Firm and Individual/HUF respectively.

Taxable Income

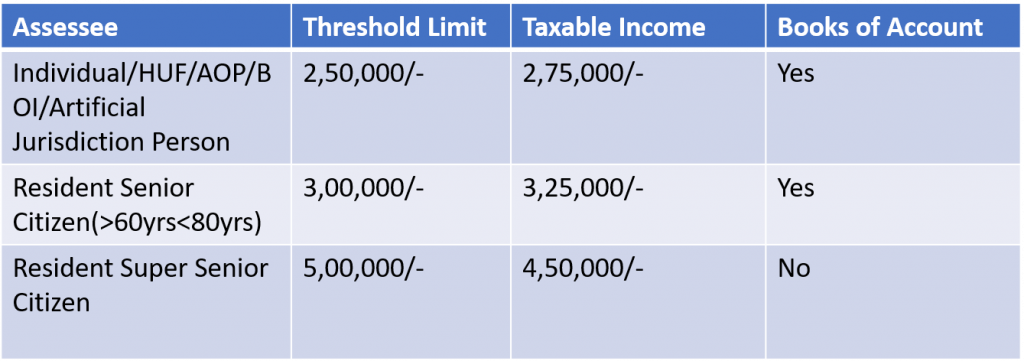

Taxable Income is calculated after considering all Incomes from Salary, House Property, Capital Gains, Business and Profession and Income from Other Sources. If the Taxable Income exceeds the basic exemption limit, then Books of account have to be compulsorily maintained.

Example of Taxable Income eligibility for preparation of books of account,

Basic Exemption Limit

Basic Exemption Limit is the limit as per Income Tax Act, a maximum amount/income limit, up to which income is not chargeable to tax,

For Individuals, Senior citizen, super senior citizens, Basic Exemption Limit is Rs.2,50,000/-, RS.3,00,000/-, Rs.5,00,000/- respectively.

Basic exemption limit for HUF/ AOP/ BOI/ Artificial Juridical Person is Rs.2,50,000/-

For Partnership firms, Companies, there is no basic exemption limit. Business Income of even Re.1 is offered to tax.

5 steps to Accounting Independence

- Download your Bank Statements and ledgers in excel format.

- Classify debits and credits in bank statement as per your expenses and incomes.

- Rework the presentation of bank statement as per software requirement by just shifting the columns.

- Import the bank statement in the software with just 1 click.

- Your Books of account are now ready.

You will be able to prepare your Computation of Income based on your books of account prepared and Business Income determined as above in the following way,

Computation of Income

The Income is computed after considering all incomes earned during the year. The total of all incomes from Salary, Rental Income, Interest Income, Short Term or Long Term Capital Gains, Business Income are presented in the Computation of Income to determine total income and tax liability.

Conclusion

Preparation of Books of Account is mandatory in the majority of cases and hence accounting independence will help you save respective penalties and ensure 100% statutory tax compliance.

Do follow my blog to learn more about Accounting for Equities Futures Derivative Trading(F&O), prepare computation of Income, and save interest , and presentation of Futures Derivative Income in your Return of Income(ITR), thereby achieving Accounting Independence.

In next article , You will learn to prepare your books of account, practically on free versions of professional software such as Tally ERP9, Zoho Books and Win man.